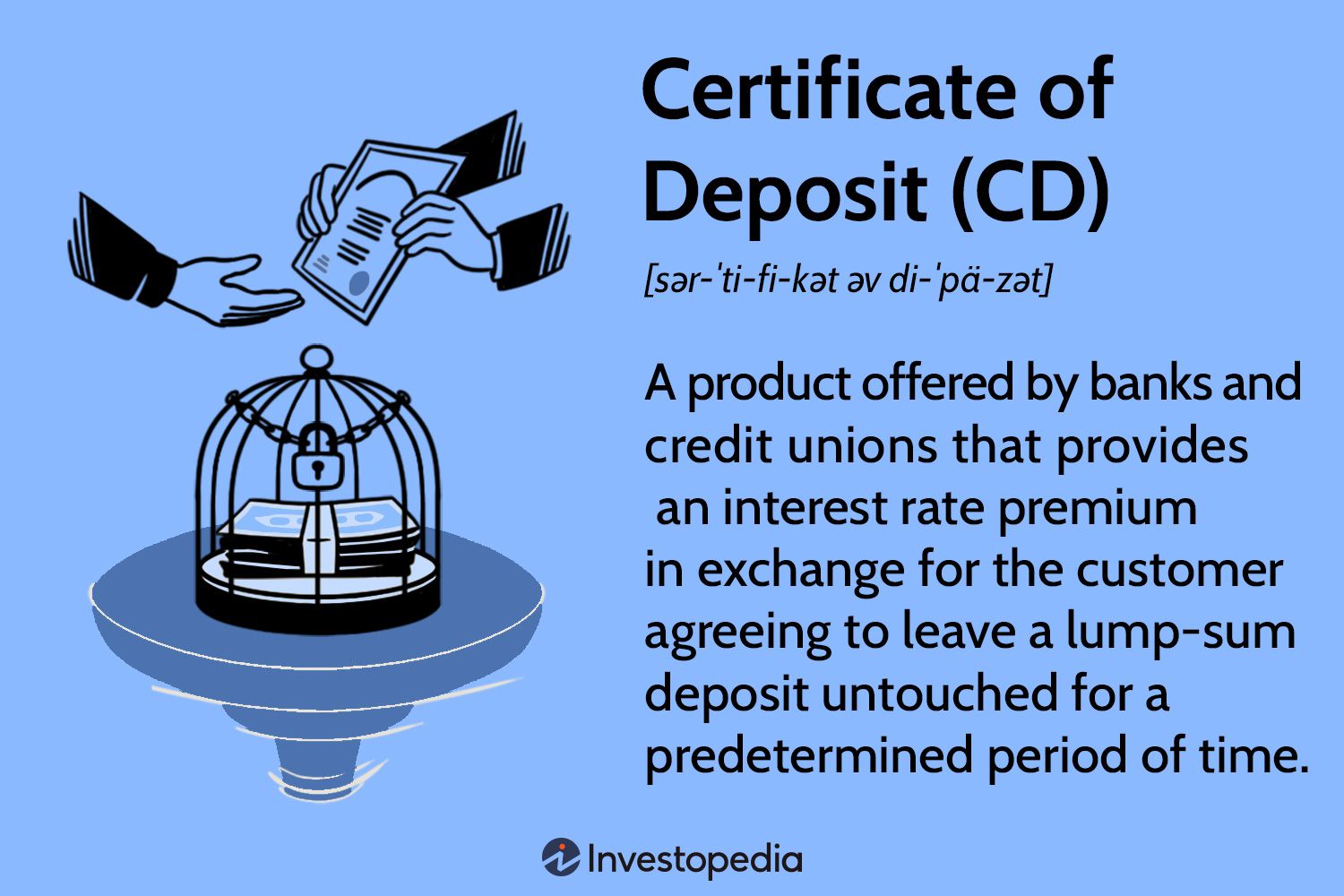

Certificate of Deposit (CDs)

Learn all about various types of certificates of deposit, how they work and how they potentially fit into your savings and investment planning. Browse Investopedia’s expert-written library to learn more.

Best CD Rates

Guide to CDs

-

Can you build credit with CDs?

CDs, along with other types of deposit products, do not build credit. Only borrowing money through some type of loan from a financial services lender that reports to credit bureaus, like with a car loan, personal loan or credit card, can build a credit history.

-

Are CDs different from U.S. savings bonds?

Yes, CDs are different from U.S. savings bonds in that CDs are a deposit account that have a fixed term held with commercial banks and U.S. savings bonds are debt obligations of the United States federal government. U.S. savings bonds also offer fixed terms that pay interest at maturity but provide longer term options compared to traditional CDs.

-

How can an individual invest with certificates of deposit?

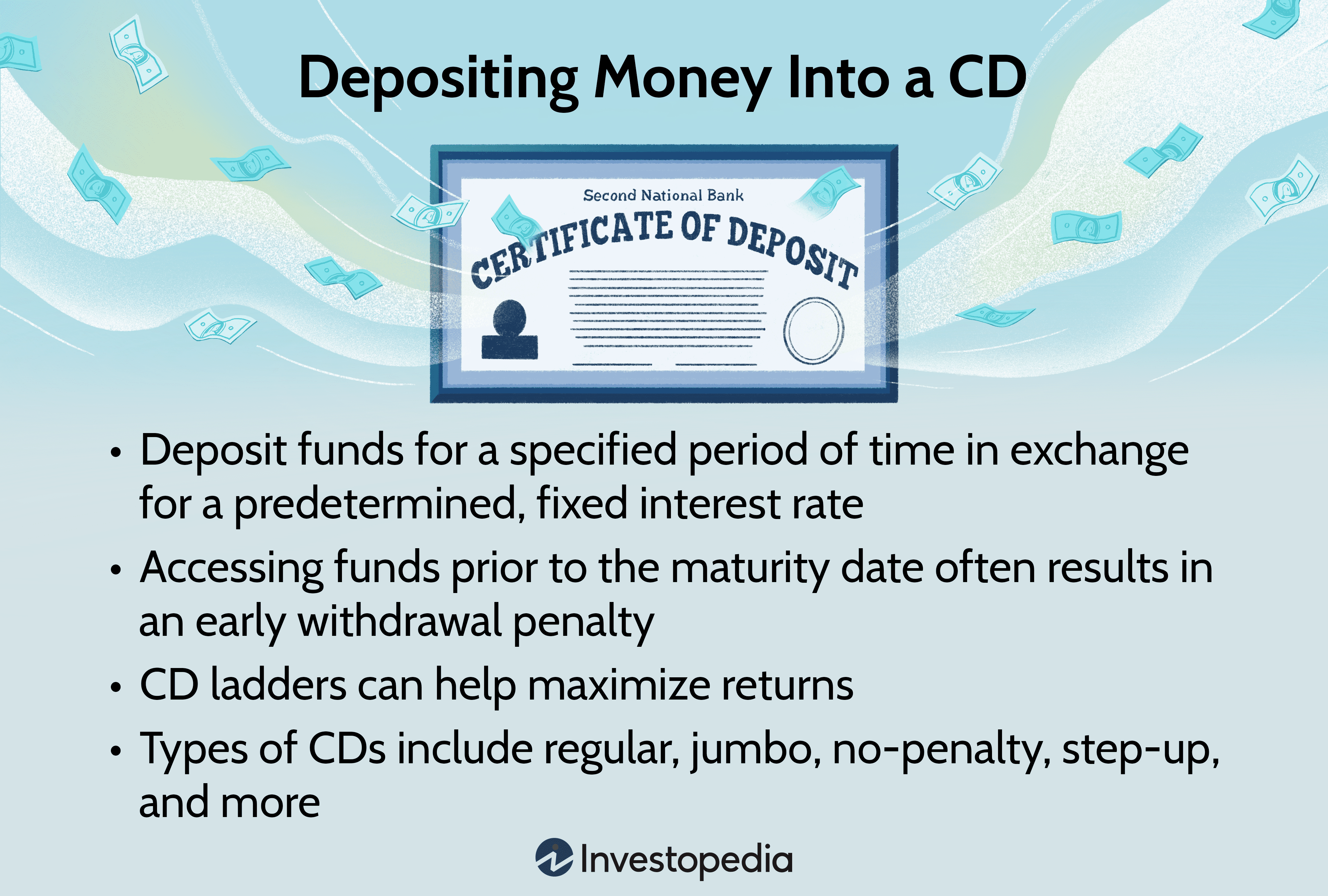

Investable funds can be deposited in certificate of deposit instruments of various terms with commercial banks, where they will earn fixed or variable interest that is payable at maturity.

Learn More How to Invest With CDs -

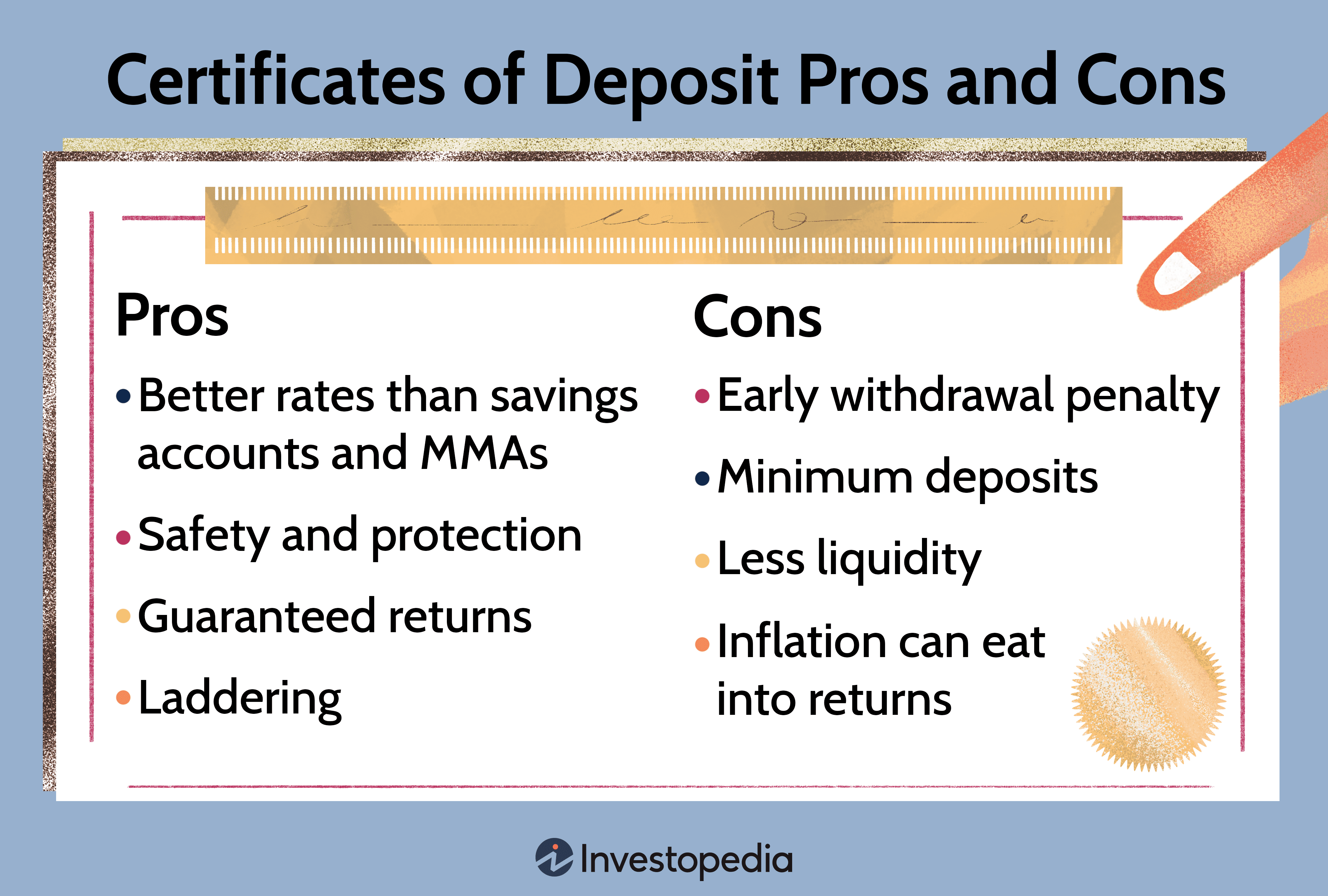

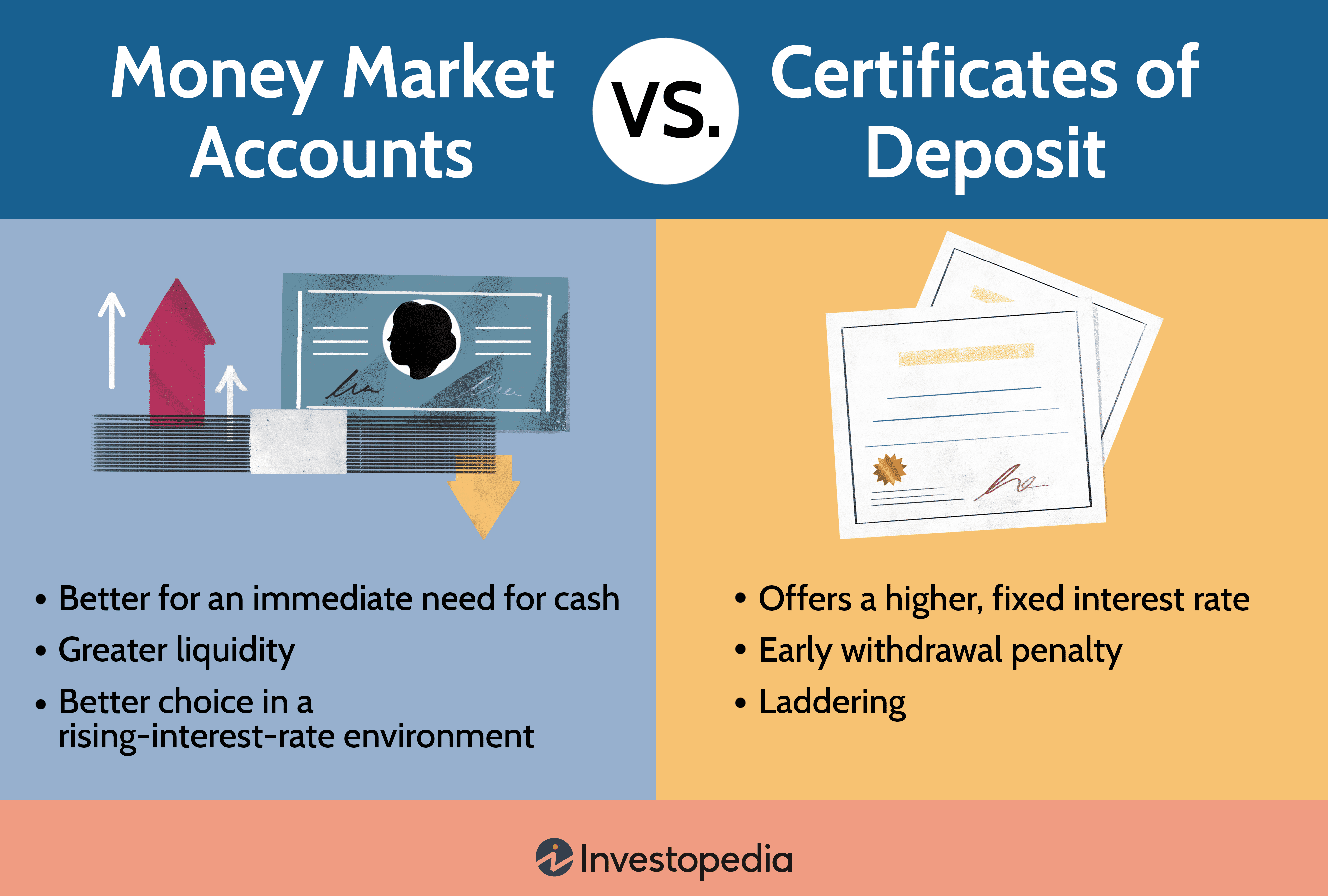

Which is a better savings option - CDs or Money Market Savings?

Certificates of deposit typically pay higher interest than money market savings accounts due to the fact that they are less liquid and involve a penalty for early withdrawal. Money market savings accounts allow for limited withdrawals but do not have a maturity date or early withdrawal penalty involved. The better option depends on whether yield maximization or flexibility is more important to your financial needs.

Key Terms

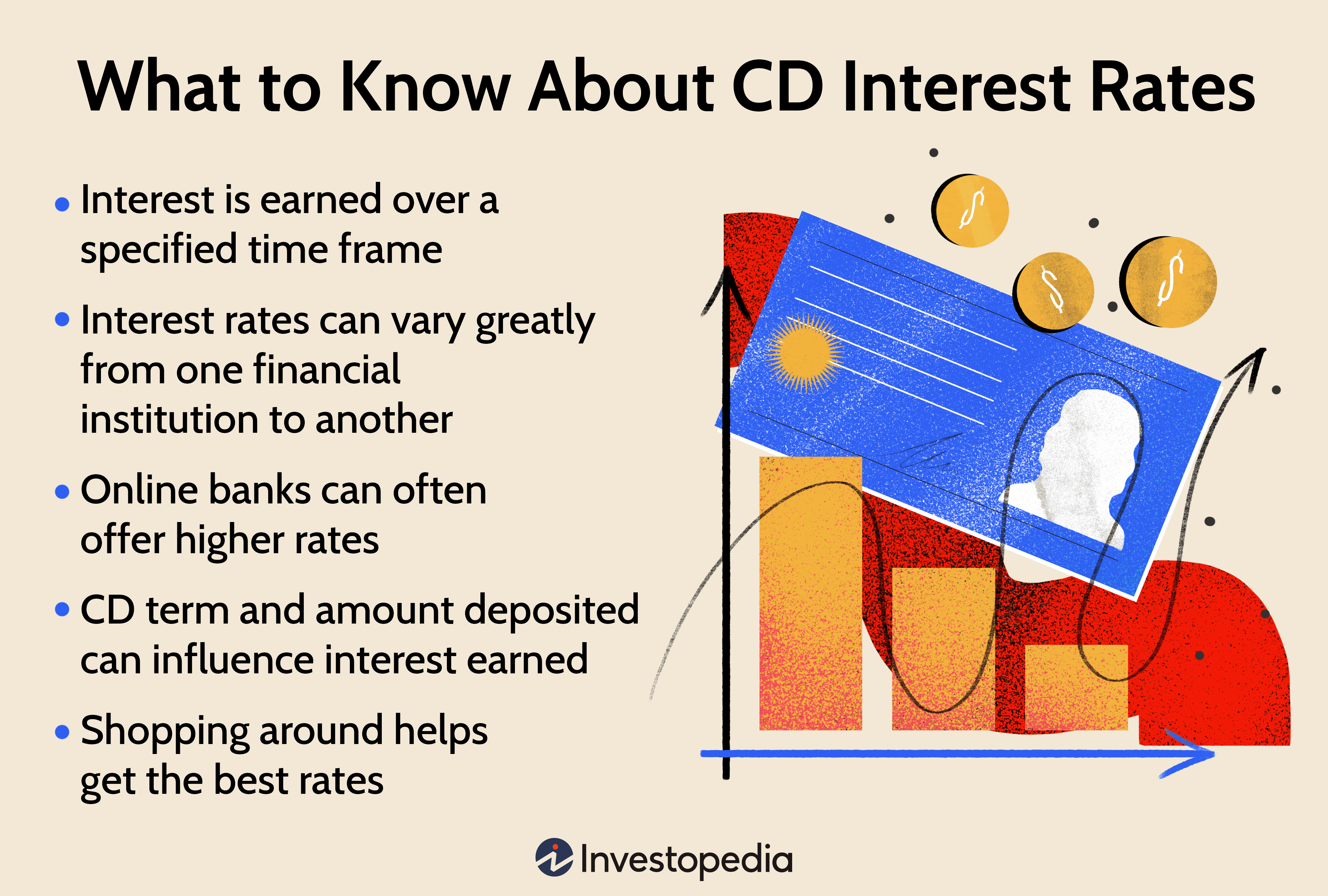

- Fixed-Rate Certificate of Deposit (CD)

A fixed rate certificate of deposit is a CD that has a set or fixed interest rate that is paid over the entire term of the instrument. The total fixed interest earned along with the CD principal is paid to the investor once the certificate of deposit reaches maturity.

- Variable-Rate Certificate of Deposit (CD)

Variable rate CDs are deposit instruments that have a fixed term but pay a variable rate of interest over the term of the instrument that can be based on an index like the prime rate. Upon maturity the principal and variable interest earned are paid to the depositor.

- Jumbo Certificate of Deposit (CD)

A jumbo certificate of deposit is a CD that has a larger minimum deposit, which is $100,000, compared to regular CDs. Traditional certificates of deposit typically have a minimum deposit of $2,500. As with traditional certificates of deposit, interest earned is paid at maturity along with return of the principal.

- Add-On CDs

An add-on CD is a type of certificate deposit that allows for additional deposits to be made before maturity of the instrument. Most CDs do not allow additional deposits to be made, however, and require a lump sum deposit at the beginning of the CD term. Add-on CDs typically pay lower interest compared to traditional CDs in exchange for the flexibility that they offer.

- CD Ladder

A CD ladder is when a depositor spreads their deposits over number of certificates of deposit across multiple maturity periods, with each successively longer maturity term representing the ascending rungs of a ladder. Using this approach reduces the risk associated with interest rate fluctuations over time by allowing the depositor to continually roll over shorter term CDs and reinvest longer term CDs as they reach maturity in order to optimize yield.

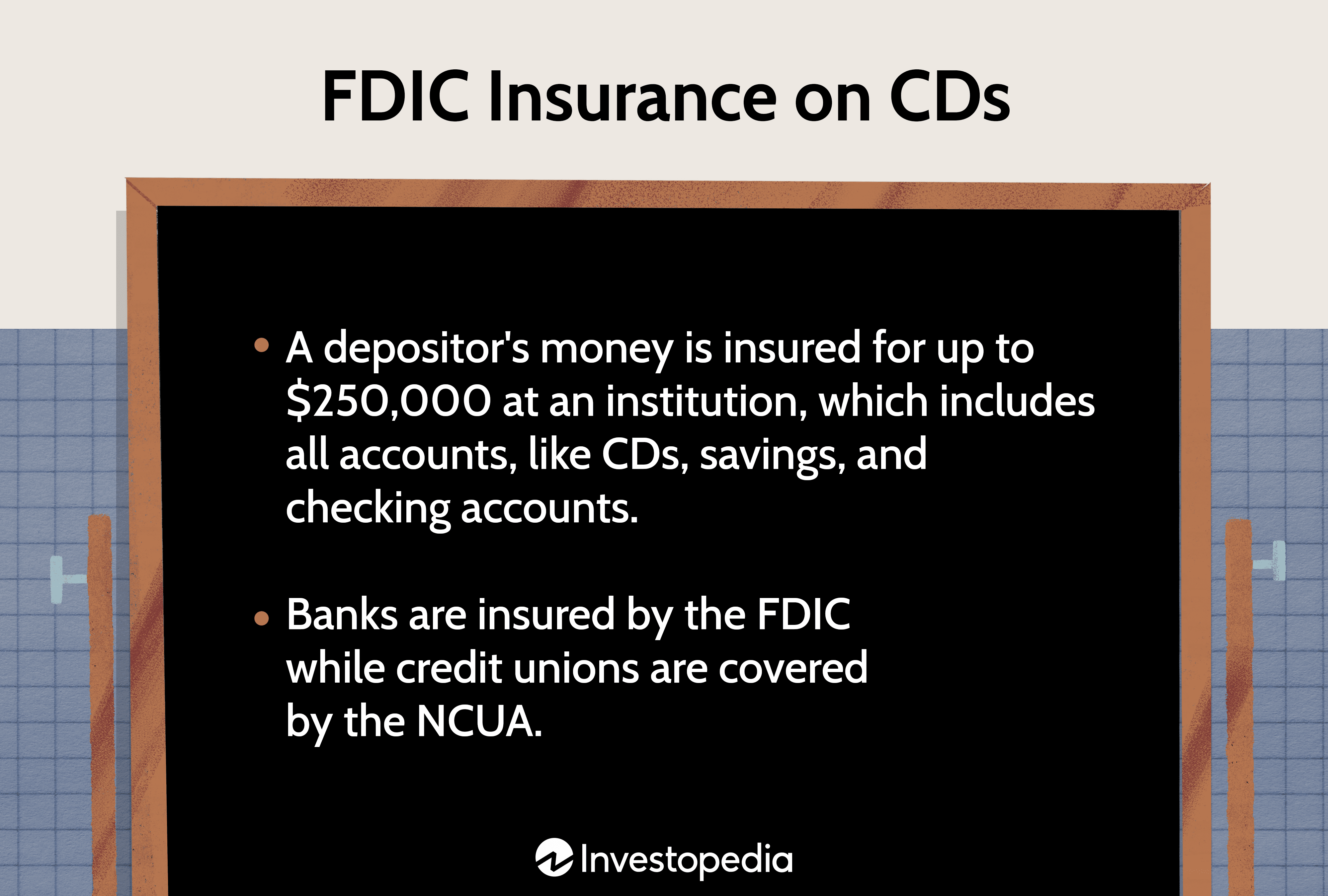

- Uninsured Certificate of Deposit

Uninsured certificates of deposit are CDs that are not covered by Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Association (NCUA). These types of CDs pay higher interest rates to investors due to the higher risk they present. Uninsured CDs are offered by investment firms and foreign banks that are not eligible for insurance coverage.

- Brokered Certificate of Deposit (CD)

Brokered CDs are offered to investors through investment firms and are technically not insured by the FDIC. However, the savings held by the investment firm with a commercial bank, from which the brokered CDs are created, are insured, which offers investors a degree of protection. Brokered CDs offer investors more flexibility and higher yields vs. traditional certificates of deposit but also present higher risk.

- Liquid Certificate of Deposit (CD)

A liquid certificate of deposit is a type of CD that allows the investor to make withdrawals before the CD reaches maturity without incurring an early withdrawal penalty. Traditional certificates of deposit do impose early withdrawal penalties so liquid CDs offer much more flexibility, although they pay less interest in exchange for that flexibility.